Financial Literacy: A New Core Subject? - Prodigy Education

How well are we preparing the next generation to navigate their financial futures? As some jurisdictions, such as Ontario, Canada implement a new financial literacy requirement for high school students, a pressing question emerges: Should financial education be a mandatory part of school curricula?

To answer this, we surveyed 1,000 American parents about their views on financial literacy education for their children. From the ideal age to start learning about money to the specific topics parents deem crucial, this study uncovers insights that could reshape how we approach financial education in schools.

Key Takeaways

- More than 9 in 10 parents believe financial literacy should be a mandatory part of their children's schooling, with budgeting being the most important topic.

- 3 in 4 parents believe financial literacy should begin as early as elementary school.

- 58% of parents think financial education is a shared responsibility between the parents and the education system.

- 86% of parents teach financial literacy at home, and 67% incentivize their children with money for chores and household tasks.

- 84% of parents are willing to sacrifice time from other subjects to accommodate financial literacy lessons; 43% would cut foreign language classes.

Early Financial Education

Financial literacy has become an increasingly important topic in education. This section explores parents' views on when and how financial concepts should be introduced to children.

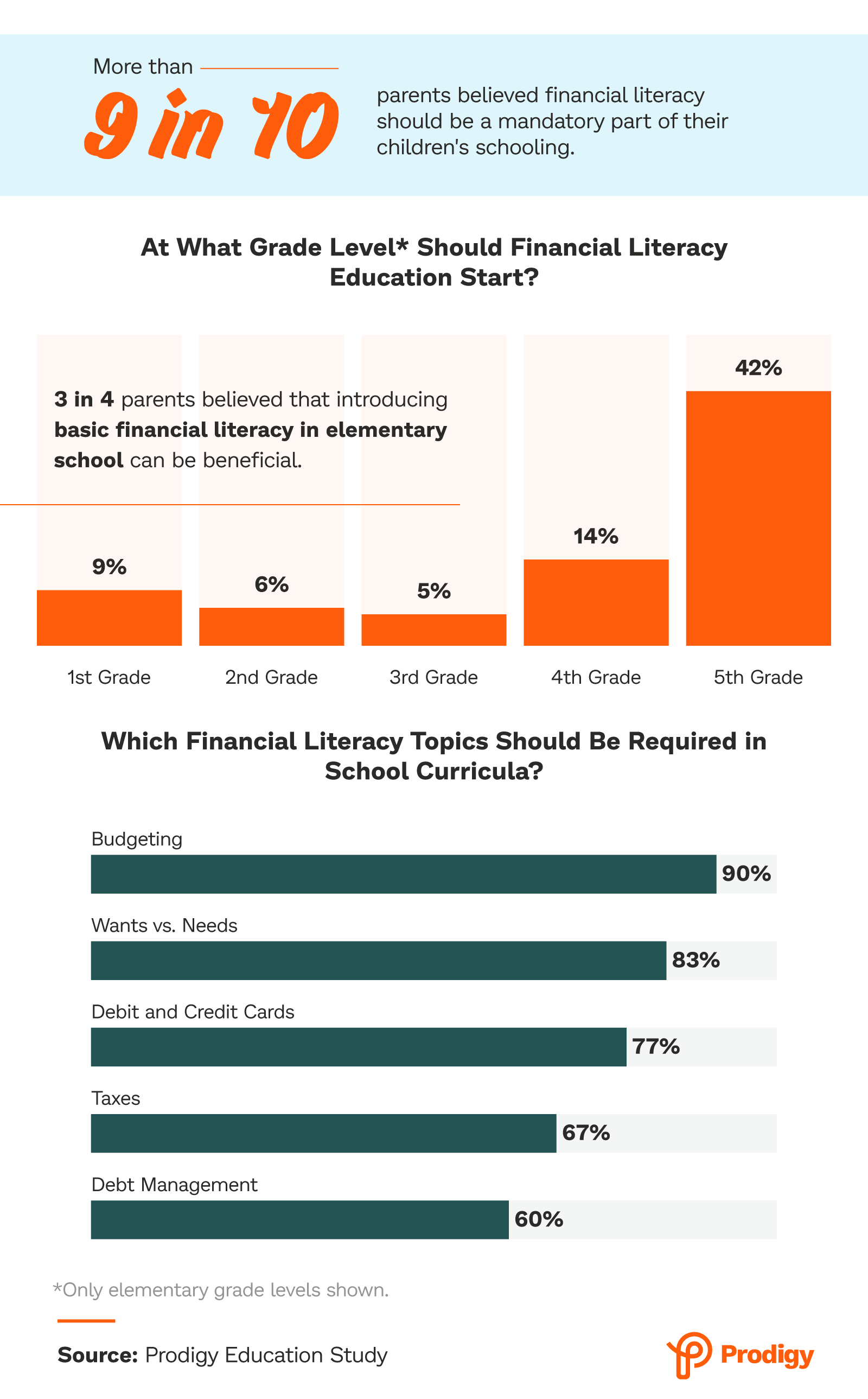

More than 9 in 10 parents believed financial literacy should be a mandatory part of their children's schooling. Three-quarters of parents also said introducing basic financial literacy in elementary school can be beneficial.

So, when exactly should kids start learning about finances? When asked about the ideal grade level to introduce it, most parents favored later elementary years. Here's how parents ranked the appropriate elementary grade levels for teaching financial literacy:

- 1st grade: 9%

- 2nd grade: 6%

- 3rd grade: 5%

- 4th grade: 14%

- 5th grade: 42%

Parents identified the following key topics they believed should be mandatory in financial literacy programs:

- Budgeting: 90%

- Wants vs. needs: 83%

- Debit and credit cards: 77%

- Taxes: 67%

- Debt management: 60%

Shared Responsibility & Money Topics

Next, we examine the roles parents believe they and educational institutions should play in teaching children about money management, and what topics these lessons should include by grade level.

Many parents (58%) viewed financial education as a shared responsibility between themselves and the education system. However, 39% believed that their children's financial education was primarily their own responsibility. Regardless of where they thought the main responsibility lay, a significant 86% of parents reported teaching their children financial literacy at home.

Parents believed different financial topics should be introduced at various school levels.

At the elementary school level, parents focused on the following fundamental concepts:

- Wants vs. needs: 71%

- Economic principles: 29%

- Debit and credit cards: 24%

- Taxes: 16%

- Debt management: 12%

For middle school students, parents favored these money management skills:

- Budgeting: 78%

- Wants vs. needs: 76%

- Debit and credit cards: 59%

- Taxes: 37%

- Economic principles: 35%

High school curricula, according to parents, should cover the following topics, some of which are more complex:

- Taxes: 83%

- Debit and credit cards: 81%

- Credit scores: 80%

- Loans and interest rates: 79%

- Wants vs. needs/Budgeting (tie): 77%

Banking Milestones

Many parents take an active role in teaching their children about money through hands-on experiences. We asked parents to share how they involve their children in financial activities and their views on when children should access various financial tools.

Two-thirds of parents (67%) reported using money as an incentive for kids to do chores. These parents encouraged their children to save an average of 35% of their earnings, providing a practical lesson in budgeting and saving.

We also found that many children have access to savings accounts from an early age. The percentage of kids with savings accounts increased with age:

- Elementary school: 57%

- Middle school: 71%

- High school: 78%

Credit card access, however, was more limited. Here are the percentages of parents whose children were using credit cards by grade level:

- Elementary school: 6%

- Middle school: 11%

- High school: 22%

When asked about the appropriate age for children to access various financial tools, parents provided the following ages (shown as averages):

- Checking/savings account: 12 years old

- Debit card: 15 years old

- Credit card: 19 years old

Making Room for Money Lessons

Integrating financial literacy into school curricula raises questions about its impact on other subjects. This section explores parents' perspectives on balancing financial education with existing academic programs.

Nearly 95% of parents were confident that their children would maintain their performance in other academic subjects if financial education became a part of the curriculum. The importance parents place on financial education was also apparent in their willingness to make trade-offs: 84% said they'd sacrifice time from other subjects to accommodate financial literacy lessons.

When asked which classes they would be willing to cut to make room for financial education, parents identified the following subjects:

- Foreign language: 43%

- Music: 36%

- Art: 33%

- Physical education: 33%

- History: 19%

The Case for Mandatory Financial Education

Most parents advocated for financial education in schools, and many were willing to sacrifice time from other subjects. This finding means that financial literacy is now seen as a fundamental rather than an optional skill. Parents' preference for the early introduction of financial concepts, coupled with the emphasis on practical skills like budgeting, reveals a need for a comprehensive, age-appropriate financial curriculum.

This study provides insights to help educators and policymakers develop financial education programs that align with parental expectations and prepare students for real-world financial challenges. Prioritizing financial literacy is an investment in their future financial well-being, empowering them to make informed decisions that will shape their lives and our economy for years to come.

Methodology

For this study, we surveyed 1,000 American parents about including financial literacy in their children's curricula. The average age was 44. Generationally, 6% of respondents reported as baby boomers, 21% as Generation X, 51% as Millennials, and 22% as Generation Z.

About Prodigy Education

Prodigy Education is a global leader in game-based learning. Our mission is to help every student in the world love learning, motivating millions worldwide via fun, secure, and accessible curriculum-aligned gameplay experiences. At Prodigy Education, we believe maximizing student motivation helps develop a lifetime love of learning. Prodigy's approach to fun, game-based learning means kids no longer have to choose between homework and playtime. Visit www.prodigygame.com to learn more.

Fair Use Statement

Noncommercial repurposing of this content is encouraged. When sharing, please link back to this page as the original source.